Shocked and yet not surprised. Sounds like a contradiction, or perhaps a very conflicted person in a confusing circumstance. It is long been known by some of us who actually take the time to question the dominate paradigm (as opposed to just googling stuff to support one’s bias) that government agencies deceive their citizens, violate the constitution and the rights of those same citizens, and use violence to enforce their unlawful edicts.

The U.S. Treasury, it’s counter part “The FED”, and it’s police (the IRS) are no exceptions. In really, they are the worse of all offenders globally. They look at citizens as milk cows to be drained, but they are really more like parasites that are slowing killing the host, which by the way, is you and me.

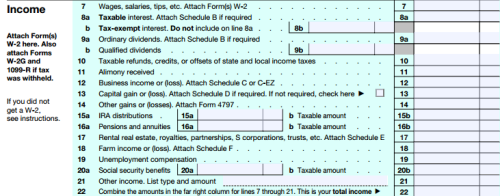

For instance, did you know that your wages, salaries, or compensation for your labor or product is not the same as your income? I bet you did not. But the IRS 1040 makes it look like it is which is in direct defiance to various supreme count rulings. What rulings you ask? Well how about these…

“If there is no gain, there is no income.” [1] …It [income] is not synonymous with receipts. Simply put, pay from a job is a ‘wage,’ and wages are not taxable. Congress has taxed income, not compensation.” United States Supreme Court Conner v. United States. 303 F. Supp. 1187 (1969) pg. 1191: 47 C.J.S. Internal Revenue 98, Pg. 226. (Emphasis added).

Read it carefully, WAGES ARE NOT TAXABLE, and Congress has taxed income, not compensation. Well that was pretty clear. How about this…

“The claim that salaries, wages, and compensation for personal services are to be taxed as an entirety and therefore must be returned by the individual… is without support, either in the language of the Act or in the decisions of the courts construing it… it is not salaries, wages or compensation for personal services that are to be included in gross income. That which is to be included is gains, profits, and income derived from salaries, wages, or compensation for personal services.” United States Supreme Court, Lucas v. Earl, 281 U.S. 111 (1930). (Emphasis added).

The act referred to in the above quote is the infamous 16th Amendment, which is a topic for some other day.

Now for sure the government has tried to force another meaning on the language by trying to get the court to support the pillage and impoverishment of the American people by trying to fold all earnings (everything that comes in) as gross income. That was also struck down.

“We must reject in this case…the broad contention submitted in behalf of the Government that all receipts – everything that comes in – are income within the proper definition of the term ‘gross income’…” United States Supreme Court Doyle v. Mitchell Brother, Co., 247 US 179 (1918).

And the IRS code still defines gross income correctly (as of this research) in IRS code Section 22 GROSS INCOME:

(a): Gross income includes gains, profits, and income derived from salaries, wages, or compensation for personal service…

All this should be painfully clear. The wages you earn is compensation for you time and labor. It is not income according the the 16th Amendment and the Supreme Court. Income (which are the same as gains and profits) is derived from your compensation, not the same as your compensation. When I get paid, which is my compensation or my wages or salary, I pay my mortgage, I buy food, put gas in my car, I pay the utility bills, I go to the movies, etc. All that is not income to be taxed. What is to be taxed is if I take what ever is left over and invest it and make a return on it (that is I make a profit or gain from that investment) that is what is taxable. This is very plain and clear.

So why is the IRS 1040 built so incorrectly? It is intentionally designed to give you the false impression that wages, salaries, compensation are synonymous with income. This is in clear defiance to the Supreme court and the 16th amendment.

Also, 1099’s shouldn’t be in there either, that is also compensation, not income. (See what-is-income).

As long as people remain unaware of this, the government can continue to borrow money for its wars and for buying votes (welfare) and to fund its police and surveillance state. When this theft stops, the FED stockholders won’t get there 6% dividend.

I hope you do know that most of your taxes go to support the federal governments borrowing schemes, not to build roads and bridges. They have to borrow and tax you to pay the banks the interest due for this borrowing, and to cover benefits and pensions so the bureaucrats, courts and law enforcement will continue to do there biding.

This endless borrowing is a major reason why MRI’s are many thousands of dollars when the true cost is $100 as in Japan, or why a hospital bed is $1500 a night for a shared room but a four star hotel runs $200 in the god-forsaken town of Washington DC. (See The Market Ticker ) Government and the FED have driven everything sky high then they come to the rescue with something like EBT cards. Government is the disease masquerading as the cure. If that doesn’t work they lead us to war against a scapegoat.

To be far, perhaps TurboTax, TaxAct, H&R Block and TaxSlayer are just trying to get you to fill out the form the way the IRS expects you to. Or perhaps they are counting on the deception to continue so the dominate paradigm will continue? If it stops, so does their revenue.

One more thing. To the American Christian you unthinkingly quotes “Render to Caesar what is Caesar’s”. If you understood your own law and history, you would know that what is due Caesar is the tax on the profit or gain (income) from wages, not tax on the wages themselves. Yes, you have to pay your lawful taxes, not unlawful ones, which is what we have been doing.

“The Constitution of these United States is the supreme law of the land. Any law that is repugnant to the Constitution is null and void of law.” Marbury v. Madison, 5 US 13

Stop taking the blue pill

References…

Conner v. United States, 303 F. Supp. 1187 (S.D. Tex. 1969)

http://law.justia.com/cases/federal/district-courts/FSupp/303/1187/1623533/

Lucas v. Earl 281 U.S. 111 (1930)

https://supreme.justia.com/cases/federal/us/281/111/case.html

Doyle v. Mitchell Bros. Co. 247 U.S. 179 (1918)

https://supreme.justia.com/cases/federal/us/247/179/case.html

Read Full Post »

{kind=link}